Amongst the sectors, the biggest loss was posted by the Commercial Banking sub-index (-3.38%) as stocks of Standard Chartered Bank (-Rs 45) and Nabil Bank (-Rs 180) succumbed to intense supply pressure. Kuber Merchant Finance (-Rs 392) which is adjusting its price post book closure dragged down the Finance Company sector (-1.91%). Despite NDEP Bank (+Rs 18) posting the second highest weekly gain, the Development Banking sector (-1.97%) failed to impress as Sahayogi Vikas Bank (-Rs 70) experienced price readjustment. Siddhartha Development Bank´s Promoter Share (-Rs 93) traded after a long gap. Similarly, the ´Others´ sector (-1.80%) ended in the red zone as Nepal Telecom (-Rs 9) shed value. However, the Hydropower sector (+1.76%) defied the market trend with appreciation in the share prices of Chilime Hydropower (+Rs 50). Sagarmatha Insurance (+Rs 72) and Shikhar Insurance (+Rs 25) topped the gainers´ chart pulling up the Insurance sector (+1.20%). SEBON, the regulators, announced that CDS will be implemented in approximately eight months following an agreement signed between Nepal Stock Exchange and Central Depository and Service (India) Limited on January 17. SEBON has also revised the Securities Registration and Issue Regulation by putting a cap of 5% on public share allotment to local residents in hydropower and manufacturing projects.

Siddhartha Finance withdrew its merger plan and canceled the proposed 1:3.83 right issue, and is instead issuing 2:1 rights shares. International Leasing and Finance company (+Rs 0) has extended its rights issue closing date from January 18 to February 5 . Annapurna Bikas Bank (-Rs 10) is closing its books on January 29 for a 1:2.2 rights issue while Paschimanchal Development Bank (-Rs 120) is closing its books on 26 January a 1:2.1 right issue.

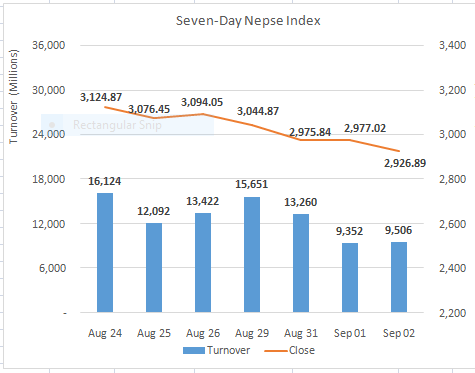

On the IPO front, Kasthamandup Development Bank has allotted its IPO. Technical analysis signals that the downtrend will linger as the market continues to experience persistent supply pressure.

Related story

Understanding Stock Market